December, 2017

The Tax Cuts and Jobs Act legislation was signed into law on December 22, 2017. The Act makes extensive changes that affect both individuals and businesses. Some key provisions of the Act are discussed below. Most provisions are effective for 2018. Many individual tax provisions sunset and revert to pre-existing law after 2025; the corporate tax rates provision is made permanent. Comparisons below are generally for 2018.

INDIVIDUAL INCOME TAX RATES

Pre-existing law. There were seven regular income tax brackets: 10%, 15%, 25%, 28%, 33%, 35%, and 39.6%.

New law. There are seven tax brackets: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. These provisions sunset and revert to pre-existing law after 2025.

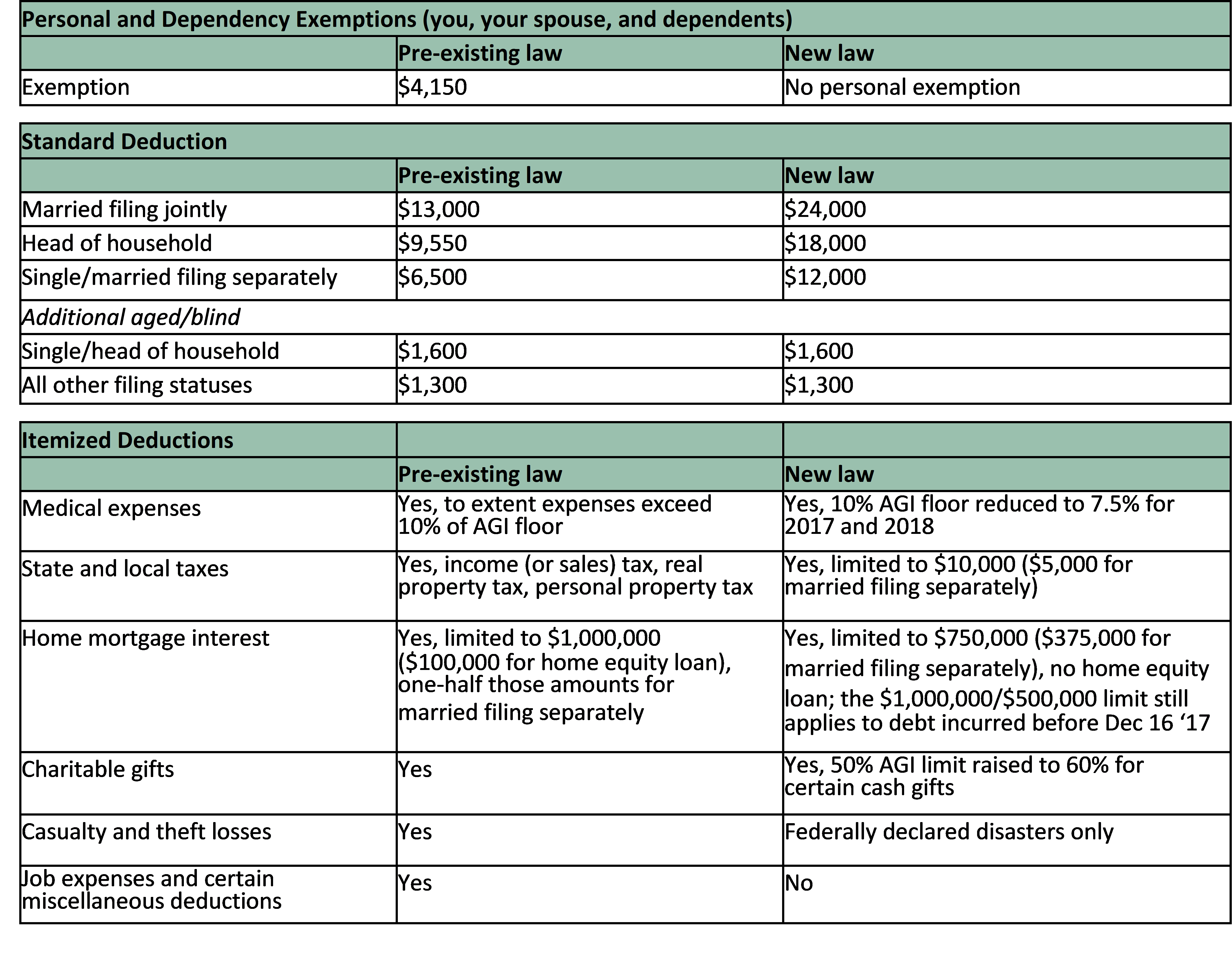

STANDARD DEDUCTION, ITEMIZED DEDUCTIONS, AND PERSONAL EXEMPTIONS

Pre-existing law. In general, personal (and dependency) exemptions were available for you, your spouse, and your dependents. Personal exemptions were phased out for those with higher adjusted gross incomes.

You could generally choose to take the standard deduction or to itemize deductions. Additional standard deduction amounts were available if you were blind or age 65 or older.

Itemized deductions included deductions for: medical expenses, state and local taxes, home mortgage interest, investment interest, charitable gifts, casualty and theft losses, job expenses and certain miscellaneous deductions, and other miscellaneous deductions. There was an overall limitation on itemized deductions based on the amount of your adjusted gross income.

New law. The standard deduction is significantly increased, and the additional standard deduction amounts for those over age 65 or blind are still available. The personal and dependency exemptions are no longer available.

Many itemized deductions are eliminated or restricted. The overall limitation on itemized deductions based on the amount of your adjusted gross income is eliminated.

- The 10% of AGI floor for the deduction of medical expenses is reduced to 7.5% in 2017 and 2018 (for regular tax and alternative minimum tax).

- The deduction for state and local taxes is limited to $10,000. An individual cannot prepay 2018 income taxes in 2017 in order to avoid the dollar limitation in 2018.

- The deduction for mortgage interest is still available, but the benefit is reduced for some individuals, and interest on home equity loans is no longer deductible.

- The charitable deduction is still available, but modified.

- The deduction for personal casualty losses is eliminated unless the loss is incurred in a federally declared disaster.

These provisions sunset and revert to pre-existing law after 2025.

STANDARD DEDUCTION, ITEMIZED DEDUCTIONS, AND PERSONAL EXEMPTIONS

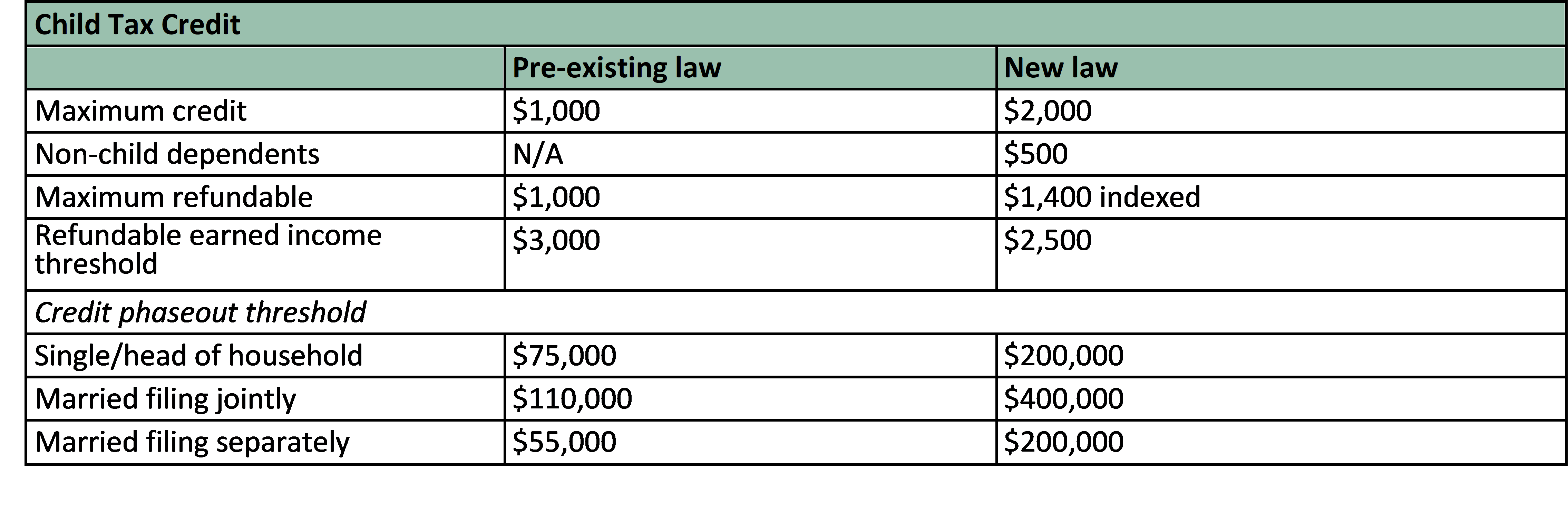

CHILD TAX CREDIT

Pre-existing law. The maximum child tax credit was $1,000. The child tax credit was phased out if modified adjusted gross income exceeded certain amounts. If the credit exceeded the tax liability, the child tax credit was refundable up to 15% of the amount of earned income in excess of $3,000 (the earned income threshold).

New law. The maximum child tax credit is increased to $2,000. A nonrefundable credit of $500 is available for qualifying dependents other than qualifying children. The maximum refundable amount of the credit is $1,400, indexed for inflation. The amount at which the credit begins to phase out is increased, and the earned income threshold is lowered to $2,500. The changes to the credit sunset and revert to pre-existing law after 2025.

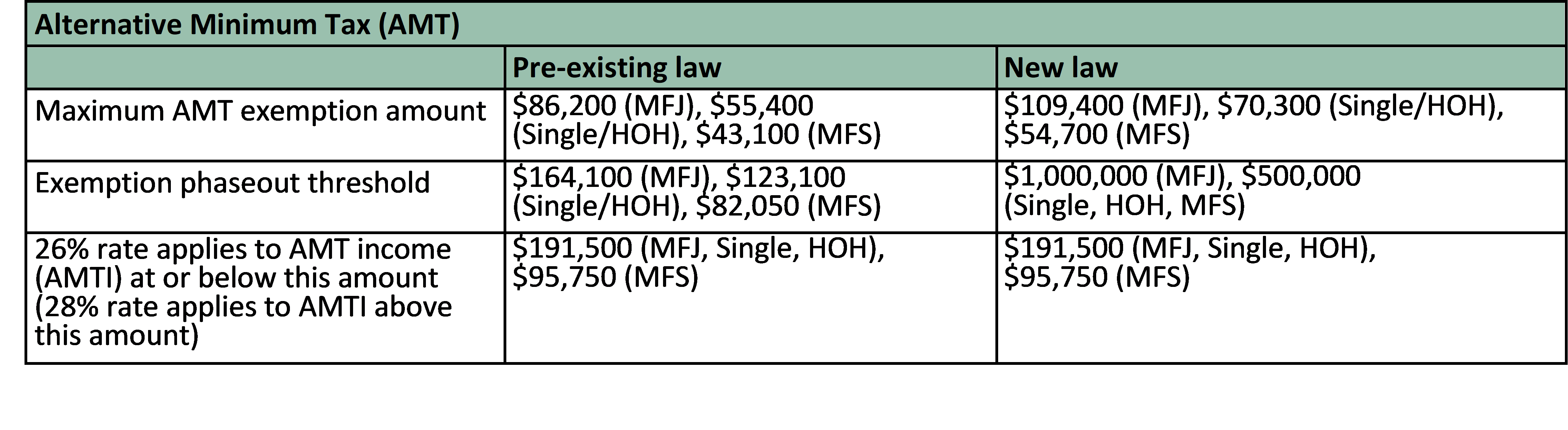

ALTERNATIVE MINIMUM TAX (AMT)

Under the Act, the alternative minimum tax exemptions and exemption phaseout thresholds are increased. The AMT changes sunset and revert to pre-existing law after 2025.

KIDDIE TAX

Instead of taxing most unearned income of children at their parents’ tax rates (as under pre-existing law), the Act taxes children’s unearned income using the trust and estate income tax brackets. This provision sunsets and reverts to pre-existing law after 2025.

CORPORATE TAX RATES

Under the Act, corporate income is taxed at a 21% rate. The corporate alternative minimum tax is repealed.

SPECIAL PROVISIONS FOR BUSINESS INCOME OF INDIVIDUALS

Under the Act, an individual taxpayer can deduct 20% of domestic qualified business income (excludes compensation) from a partnership, S corporation, or sole proprietorship. The benefit of the deduction is phased out for specified service businesses with taxable income exceeding $157,500 ($315,000 for married filing jointly). The deduction is limited to the greater of (1) 50% of the W-2 wages of the taxpayer, or

(2) the sum of (a) 25% of the W-2 wages of the taxpayer, plus (b) 2.5% of the unadjusted basis immediately after acquisition of all qualified property (certain depreciable property). This limit does not apply if taxable income does not exceed $157,500 ($315,000 for married filing jointly), and the limit is phased in for taxable income above those thresholds. This provision sunsets and reverts to pre-existing law after 2025.

RETIREMENT PLANS

Under the Act, the contribution levels for retirement plans remain the same. However, the Act repeals the special rule permitting a recharacterization to unwind a Roth conversion.

ESTATE, GIFT, AND GENERATION-SKIPPING TRANSFER TAX

The Act doubles the gift and estate tax basic exclusion amount and the generation-skipping transfer tax exemption to about $11,200,000 in 2018. This provision sunsets and reverts to pre-existing law after 2025.

HEALTH INSURANCE INDIVIDUAL MANDATE

The Act eliminates the requirement that individuals must be covered by a health care plan that provides at least minimum essential coverage or pay a penalty tax (the individual shared responsibility payment) for failure to maintain the coverage. The provision is effective for months beginning after December 31, 2018.

If you have any questions, please contact us at 210-547-3450.

* Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2017

This information, developed by an independent third party, has been obtained from sources considered to be reliable, but Raymond James Financial Services, Inc. does not guarantee that the foregoing material is accurate or complete. This information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. This information is not intended as a solicitation or an offer to buy or sell any security referred to herein. Investments mentioned may not be suitable for all investors. The material is general in nature. Past performance may not be indicative of future results. Raymond James Financial Services, Inc. does not provide advice on tax, legal or mortgage issues. These matters should be discussed with the appropriate professional.

Securities offered through Raymond James Financial Services, Inc ., Member FINRA/SIPC. S. Harris Financial Group is not a registered broker/dealer and is independent of Raymond James Financial Services. Investment advisory services offered through S. Harris Financial Group.